Parents often view funding their children’s college education as a measure of love and success. They anticipate rising tuition costs and feel an urgency to save early. This drive can become overwhelming, fueled by cultural expectations, marketing messages, and conversations with peers. It creates a common misconception that saving for college must come first—even before paying off debt, building emergency savings, or funding retirement. Such beliefs place parents at odds with foundational personal finance practices and can lead to long-term instability.

Emotional and Cultural Pressures to Fund College First

Parents often feel scrutinized by peers and relatives who ask about college savings before a child can even talk. Birthday parties include questions about 529 plans rather than the toddler’s favorite toys, sending a subtle message that not saving is negligence. Marketing campaigns show infants in graduation caps, reinforcing the idea that college planning must start in the nursery. Guidance counselors and financial institutions describe early contributions as the only path to avoid crushing student debt. These cultural cues are powerful and often override personal financial caution.

Parents internalize the message that delaying contributions makes them irresponsible, so guilt drives their decisions. They may divert money from debt payments or emergency funds to deposit into a college account. Some reduce retirement contributions to keep pace with a neighbor’s savings plan or to satisfy a grandparent’s expectations. Instead of focusing on their own financial stability, many parents focus on appearing prepared for college costs. The emotional pressure to prioritize college creates behavioral patterns that conflict with long-term financial health.

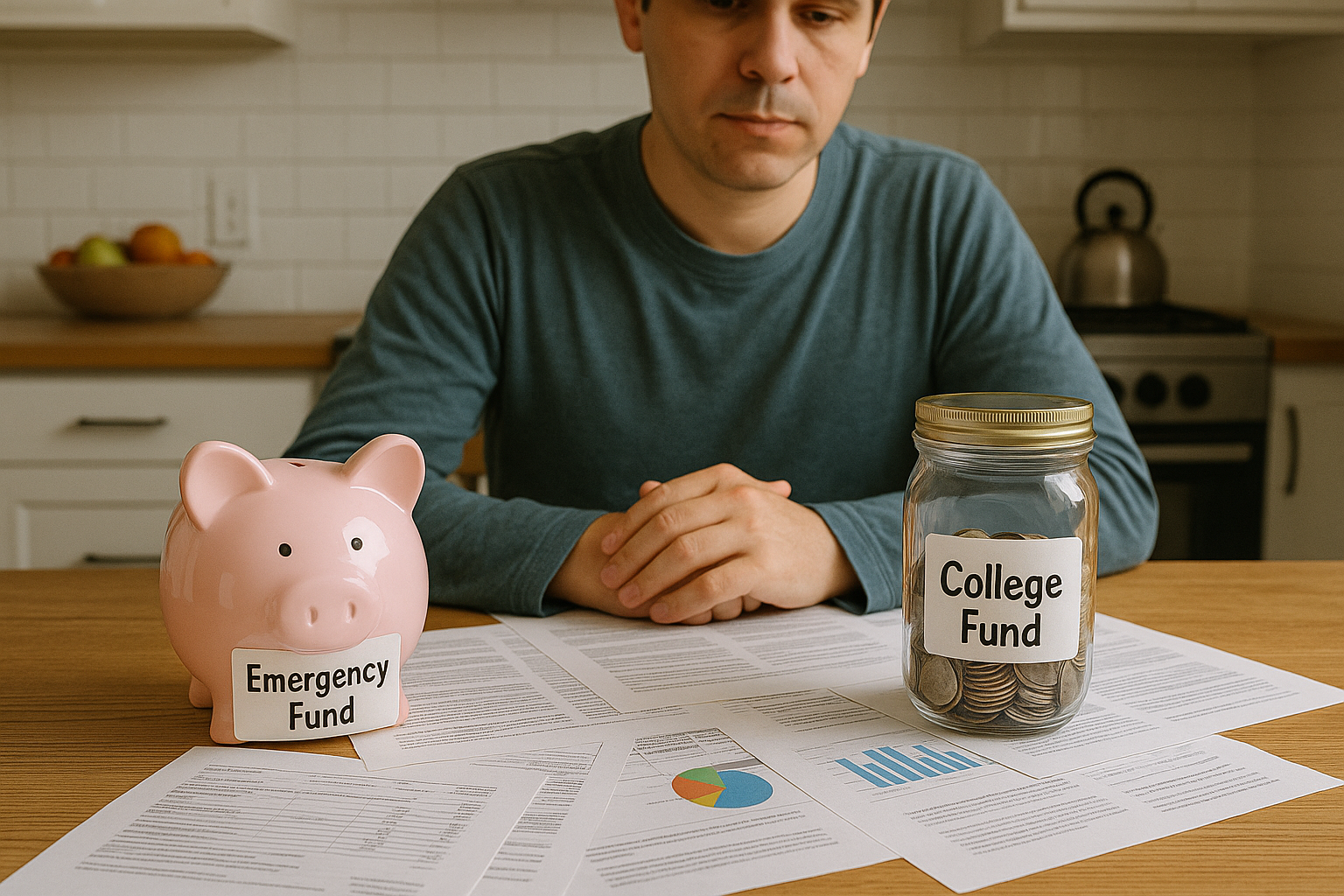

Consequences of Misaligned Timing

When parents fund college savings before eliminating high-interest debt, they pay more in interest over time. The money devoted to tuition accounts could instead reduce debt balances and free future cash flow. Underfunded emergency reserves create vulnerability to unexpected expenses like medical bills or job loss. If a major expense arises, parents may withdraw from the college account or use credit cards, erasing progress and increasing debt.

Delaying retirement contributions also has long-term ramifications, because compound growth depends on time as much as contribution size. Parents who postpone retirement investments might find themselves contributing larger sums later, or worse, working longer than planned. Even after years of sacrifice, college funds may still fall short if tuition increases outpace investments. Children may then take out loans, burdening both generations because parents often assist with repayments or co-sign for additional debt. Parents who stretch themselves to fund tuition can become financially dependent on their children later, reversing the intended support dynamic. Prioritizing college savings without stabilizing personal finances exposes families to risks that persist long after graduation day.

Structured College Funding After Stabilizing Finances

A better approach starts with sequential financial milestones: eliminating high-interest debt, building an emergency fund, and investing consistently for retirement. Once those milestones are met, parents can safely begin saving for education without jeopardizing their own security. College savings should never interrupt debt reduction or emergency funding, because those foundations protect the entire household.

When ready, parents can open a 529 plan to contribute after-tax dollars that grow tax-free and can be withdrawn for qualified education expenses. Automated monthly transfers into the plan encourage consistency and reduce the temptation to skip contributions. Families should choose low-cost, diversified investment options within the plan to balance growth potential and risk. Education Savings Accounts also offer tax benefits, although contribution limits and income thresholds require careful consideration.

After establishing the account structure, families can look for scholarships and grants to reduce the amount needed from savings. Encouraging teenagers to work part-time instills responsibility and helps cover books or living expenses, further easing the burden on the college fund. Choosing community college for general education courses or selecting in-state universities can significantly lower total tuition. Parents should discuss these cost-conscious choices with their children, explaining how they contribute to family stability and avoid debt. By following a structured plan—waiting until personal finances are secure, using tax-advantaged accounts, and making strategic education choices—families can save for college without compromising their own futures.

Helping a child pay for college is a commendable goal, but it should not come at the expense of a parent’s financial health. A robust financial foundation—free of high-interest debt, supported by an emergency fund, and strengthened by retirement contributions—makes generosity sustainable. When parents prioritize stability before college savings, they remain strong financial mentors and protect themselves from future dependency.

Once personal finances are secure, structured tools like 529 plans and Education Savings Accounts allow families to contribute meaningfully without undermining their own security. Teaching children about scholarships, part-time work, and cost-effective school choices empowers them to participate in funding their education responsibly. By sequencing generosity after personal stability and using deliberate strategies, parents can achieve both financial health and educational support for their children.

Finance Health

Focused on long-term growth and financial resilience, Finance Health is a voice of compound interest, consistency, and the long game.